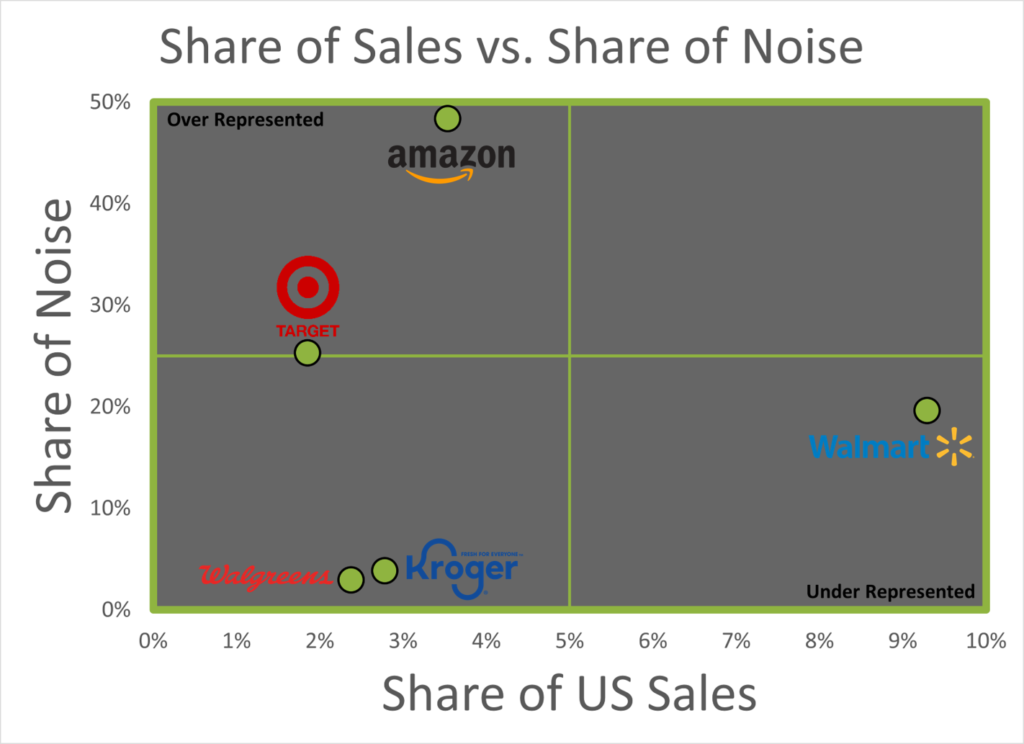

The last week in Retail featured quite a few earnings releases. Among those released were Retail’s darling (Target) and Retail’s behemoth (Walmart). When we looked at Share of Noise, these two retailers were at opposite ends of share vs noise.

And so, let’s take a look into their earnings. Down the rabbit hole* we go.

Let’s start with some numbers, shall we?

For Target:

- ID sales +22.9% (ID store + 18%, digital +50%).

- +17% traffic increase, +5% basket growth.

- Continuing to gain market share ($1BN in Q1).

- Reported EPS = $3.69 (Beat).

For Walmart:

- ID Sales +6% (digital +37%).

- -3.2% transaction quantity decline, +9.5% basket size growth.

- Gained market share in grocery; raised outlook.

- Reported EPS = $1.69 (Beat).

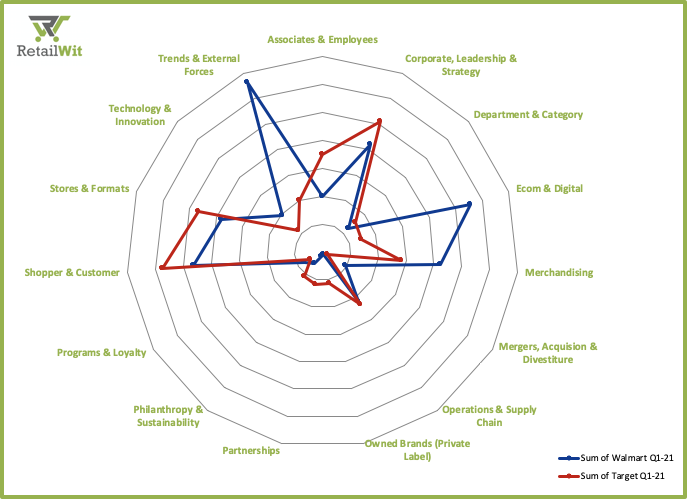

RetailWit also took a look at what they said during the earnings call (below). Walmart continues to speak to COVID19, inflation, ecommerce, and merchandising. Target continues to speak about the shopper, stores, associates, and the strategic bets they are making.

At RetailWit we believe what is said at Investor Calls is as important as the results they share. The results are a great backward indicator but what is discussed and how helps you predict where they are going. With that in mind we built a proprietary solution that types and tags the calls on our RetailWit categories, output above. Stay tuned for more info soon.

Target’s brand continues to be a strong point: Private Label experienced record sales growth (+36%). Their new CMO will be unveiling her first brand campaign tomorrow (Personally? Seems forgettable. We’ll see). The latest store-within-a-store partnership with Apple extends their brand’s halo. With 30 store openings, and 130+ remodels planned throughout 2021, Target is continuing to lean into Brick&Mortar.

Walmart’s core competency of supply chain was a strong point. Operating income increased +27%. Walmart plans on spending over $14B on OpEx (a massive increase). Executives pointed to building stronger infrastructure to support its sales volumes, particularly digital; their current volume requires a better supply chain and digital delivery platform.

There are a few key spots where each Retailer is zigging where others are zagging.

- Target is using their stores as distribution points (“…stores [are] the center of our strategy” -Brian Cornell) , whereas other retailers are relying on MFC (or CFC for Kroger). We’re also seeing the maturity of ecommerce as indicated by digital sales growth declining over time.

- Walmart, on the other hand, is doubling down on discounts (30% more discounts in stores in Q1 than prior period) as inflation increases prices. We wouldn’t be surprised if most of the cost is being passed to CPGs.

Both retailers have said they’re seeing a sharp increase in pre-pandemic buying habits (Revenge Shopping, as it has been called). So far, it appears that Target has been capturing more traffic than Walmart and has seen more robust sales growth.

Has the Darling outmaneuvered the Behemoth?

Here’s the deal: The base for Walmart (2020 US Sales: $408.9B) versus Target ($81.5B) is so drastic, Target would need to 5x the sales percentage growth of Walmart to hit an equivalent gain in revenue.

It’s not even close. Goliath wins. However… Kroger and Walgreens? They should be concerned the Bullseye is on their back.

Here’s the rest of the best – Last Week’s Top Stories.

- Remember the hilariously terrible Superbowl commercial? Oatly is laughing all the way to the bank as their shares soar 24% in the company’s IPO on Nasdaq.

- Google is doubling down on ecommerce – Google is partnering with Shopify, and have launched a new tool called the “Shopping Graph”

- Kroger’s CFO, Gary Millerchip, speaks to how Ocado is going thus far.

- Petco cited customer growth as a driver for Q1 profit, but shares didn’t jump accordingly. Could the great pet boom of 2020 be slowing down? Side note: did you know that Petco’s stock ticker is ‘WOOF’?

- Google is opening their first retail store in NYC, not far from an Apple Store. The store will highlight their phones and other gadgets.

- Amazon is consolidating their naming conventions for stores, getting rid of ‘Amazon Go’ and moving to ‘Amazon Fresh’. Seems like a small move, but you can see that Amazon is focusing on groceries – trying to stay top of mind for shoppers.

- Kohl’s had strong sales AND profit in Q1 and raised their outlook on the year. And Wall Street didn’t buy it.

- Hershey boosts better-for-you credentials with an acquisition.

- And the Chicken Wars heats up again, real (from Burger King) and faux (now featuring Drake).

*It’s a vibe, for sure.

No Comments

Leave a comment Cancel